A sweeping plan to fundamentally reshape how local governments are funded in the Sunshine State is officially heading to the voters. During a high-stakes special legislative session on June 2, 2026, lawmakers passed Governor Ron DeSantis’s ambitious proposal to dramatically lower property taxes for permanent residents.

The legislatively referred constitutional amendment passed with a supermajority, clearing the Senate in a 30-9 vote and the House in a 75-26 vote. To become law, the measure must now secure at least 60% voter approval in the upcoming November referendum.

At the LeAneSuarezGroup, we recognize that tax policies are one of the most critical factors influencing long-term property values, neighborhood affordability, and municipal infrastructure. This historic proposal represents a pivotal development for anyone who owns or plans to buy real estate on Sanibel and Captiva Islands.

In a nutshell: The Florida Legislature has cleared a constitutional amendment for the November ballot that would phase in a massive $250,000 homestead tax exemption by 2028. While proponents champion the relief for homeowners, the Lee County Board of County Commissioners has formally opposed the bill due to projected multi-million dollar local revenue shortfalls.

The Phased Exemption and What it Exempts

If approved by the public, the amendment—titled the “Save Our Homes from Excessive Property Taxes Amendment”—would dramatically increase the tax exception threshold specifically for owner-occupied primary residences.

-

The Phased Rollout: The current $50,000 homestead exemption would triple to $150,000 on January 1, 2027, and eventually climb to $250,000 on January 1, 2028.

-

The School Tax Protection: In a major late overhaul to the governor’s original wide-ranging draft, the Legislature amended the bill to ensure that the expanded exemption applies only to non-school property taxes. This vital revision completely insulates Florida’s public school districts from taking a hit to their local education funding.

Lee County Commission Signals Unanimous Opposition

Despite the built-in protections for school systems, the proposal faces heavy, unified pushback from local municipal administrations. On the exact same day the bill cleared the state capital, the Lee County Board of County Commissioners voted unanimously to send an official letter to the Legislature opposing the expanded exemption.

Local leaders note that Southwest Florida communities are still actively funding complex infrastructure and recovery projects following a string of major natural disasters, including Hurricane Ian, Hurricane Helene, and Hurricane Milton.

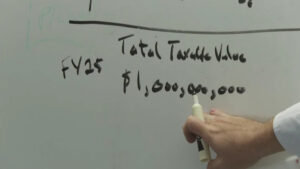

LEE COUNTY PROJECTED REVENUE SHORTFALLS

[ NEXT YEAR'S BUDGET ] ───► $129.7 Million Projected Loss

[ 2028-29 BUDGET ] ───► $240.8 Million Projected Loss

County commissioners warned state leaders that without a “stable, recurring replacement funding source” provided by the state, the bill represents one of the most volatile restructurings of local finance in Florida’s history.

The Debate: Economic Stimulation vs. Local Funding Loss

State Senator Jonathan Martin (R-Fort Myers), who has been actively consulting with local commissioners regarding their concerns, defended the bill’s placement on the ballot. While acknowledging the anxiety surrounding local budgets, Martin questioned whether the county’s steep financial loss projections adequately factored in regional marketplace expansion.

“Are they assuming that no additional homes are going to be purchased down here or that economic activity is going to stop? Economic activity increases with tax cuts. I feel very strongly that the voters should decide.”

— Sen. Jonathan Martin (R-Fort Myers)

Martin has long been a proponent of aggressive fiscal reform, having championed a legislative bill last year aimed at ordering an official state study to evaluate the total elimination of property taxes entirely.

If passed by the public this fall, the ultimate impact will require local governments—like Lee County—to carefully reassess how they balance long-term capital improvement projects against a significantly transformed tax revenue stream.